If you are a founder, finance lead, or ops lead at a growing company, your insurance portfolio is one of the few areas of spend where you are structurally disadvantaged. Policies are written in dense legal language. The broker is paid by the insurer or by your premium volume, so interests don’t fully align. The renewal cycle pressures you to accept the proposal because the alternative is being uninsured for a week.

The result is a portfolio with overlapping coverages (general liability and product liability covering the same risks), gaps that surface during a claim (“turns out our cyber policy excludes exactly the kind of breach we just had”), and premiums that have grown 30% year over year without anyone fully understanding why.

The fix is to move policy reading away from “ask the broker” and into structured analysis you can review independently. An LLM — the technology behind ChatGPT, Claude, and Gemini — pulls the key terms from every active policy. A gap-and-overlap analysis surfaces the issues. The renewal conversation starts with data rather than with the broker’s PDF.

This piece walks through the pipeline: the extraction schema, the gap-finding logic, the exposure-mapping pass that catches risks the existing policies don’t cover, and the renewal-prep workflow that turns the annual cycle from reactive into informed.

Where this fits — and where it doesn't

Use this if you have 5+ active insurance policies (general liability, D&O, E&O, cyber, workers’ comp, property, EPLI, etc.), your annual premium spend is meaningful, and the renewal conversation typically happens on the broker’s timeline rather than yours. Common fits: companies past series A, services businesses with E&O exposure, tech companies with cyber and D&O policies, organisations with significant property or workers’ comp.

Don’t use this if your portfolio is one or two simple policies (manual review is faster), you’ve delegated insurance entirely to a fractional CFO or CFO-as-a-service who handles this (their process probably already covers it), or your business has truly bespoke risk (high-end specialty insurance) where the policies are unique enough that pattern-extraction is less useful than direct legal review.

What you'll need before starting

- The active policy documents — PDFs from your broker or directly from carriers. Most brokers will send the full policy if asked; declarations pages alone aren’t enough for gap analysis.

- A model API key with long-context support — insurance policies are 30–80 pages typical, occasionally longer.

- A list of major exposures your business actually has: revenue, employee count, geographic operation, technology platforms, products / services, regulated activities. The gap-analysis compares coverage against actual exposure; without the exposure list, gaps are theoretical.

- An adviser or fractional CFO / risk manager who can validate the AI’s gap findings. The AI is an extraction and analysis layer; the judgement on which gaps matter remains human and benefits from someone with insurance domain knowledge.

Six steps to a portfolio you actually understand

- Extract coverage details with structured output — every policy, the same schema

For each policy, extract: policy type (GL, D&O, E&O, cyber, etc.), carrier, policy number, effective dates, named insureds, coverage limits (per occurrence, aggregate, sublimit by category), deductibles / retentions, key exclusions, endorsements / riders, premium, renewal date, notice-of-cancellation window. Use the structured-output features of your LLM API. Same schema across all policies makes the cross-policy comparison possible; bespoke per-policy extraction makes the analysis impossible to consolidate.

- Pull exclusions explicitly — that’s where the gaps live

Exclusions are the most operationally important section of every policy and the most commonly skipped. For each policy, extract the exclusion list with verbatim text. Common patterns to look for: war / terrorism exclusions, pandemic exclusions (post-2020 some policies added these), specific cyber-attack types excluded from cyber policies (social engineering, wire fraud), employment-practice exclusions on D&O policies. The exclusion list is what tells you what the policy doesn’t cover; the limits tell you the boundary, the exclusions tell you the holes.

- Build the coverage matrix — policy type × risk category

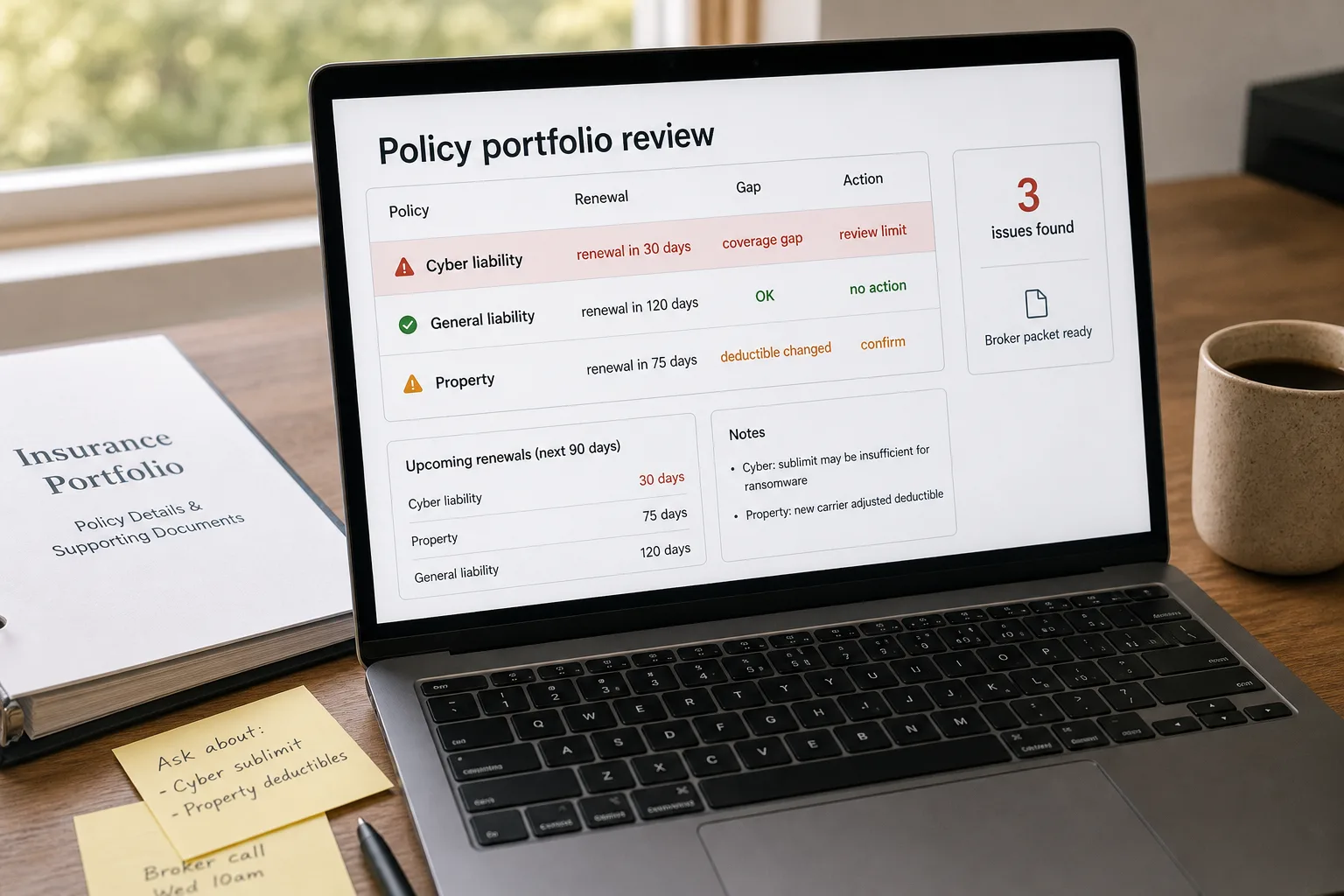

From the extracted data, build a matrix: rows are risk categories (bodily injury, property damage, intellectual property, employment practices, cyber breach, professional liability, etc.); columns are your policies; cells show which policy covers each risk (and the limits / sub-limits). The matrix makes overlaps visible (two policies covering the same risk with limits that don’t combine usefully) and gaps visible (a risk category with no policy coverage at all). Visual matrix beats narrative analysis; the matrix is what the renewal conversation references.

- Run the gap analysis — exposure vs coverage

For each major exposure in your business, check the matrix: is there coverage? Is the limit adequate for your scale? Are there exclusions that materially limit the coverage? Common gap findings: a tech company with no cyber breach-response coverage; a services company with E&O limits below the value of typical engagements; a company in multiple states whose workers’ comp lists only one state. The gap analysis surfaces these; the validation pass with the adviser converts findings into renewal asks.

- Generate the renewal-prep document — gaps, overlaps, questions for the broker

Before each renewal, produce a structured doc: identified gaps (here’s the exposure, here’s the missing coverage), identified overlaps (these two policies seem to cover the same risk, can we consolidate?), specific questions for the broker (the cyber policy excludes social engineering — what’s the cost to add that coverage?), and a benchmark of last-year coverage vs this-year proposal. The doc is the renewal conversation’s input; you walk into the meeting with the broker armed with specific questions rather than a vague sense of what’s wrong.

- Track changes year-over-year — premiums, limits, exclusions

At each renewal, store the extracted policy alongside the prior year’s. Build a year-over-year comparison: premium up X%, limit changed from Y to Z, new exclusion added. The comparison catches the silent erosions — limits that crept down, exclusions that quietly expanded, premiums that went up without a corresponding coverage upgrade. Brokers occasionally surface these; sometimes they don’t. Year-over-year tracking is what makes the renewal cycle accumulate knowledge rather than start from zero each year.

What it costs and what to expect

The gap-and-overlap findings are the operational value. The premium savings are bonus when they materialise; the strategic value is having an informed conversation with the broker about your actual risk profile.

Other ways to solve this

Modern digital insurance brokers (Embroker, Newfront, Vouch, Founder Shield). Increasingly bundle policy-portfolio dashboards that show coverage at a glance. Right answer if you’re working with a modern broker that provides this transparency. Trade-off: the dashboard reflects the broker’s view, which is helpful but not independent.

Hire a fractional risk manager or insurance consultant. For one-time portfolio reviews or pre-renewal analysis. Insurance domain expertise is genuinely valuable; the AI extraction layer complements rather than replaces it. Many teams do this annually pre-renewal as a check on the broker’s proposal.

Trust the broker, review by exception. The traditional approach. Works when the broker is excellent and aligned with your interests; less reliable as a default. Best paired with a periodic independent review (every 2–3 years if not annually) to catch drift.

Don’t review — accept whatever the broker proposes. Honest answer for very-early-stage companies where the portfolio is small and the premium spend is modest. Becomes increasingly indefensible as portfolio and premium grow; the threshold to invest in informed review is usually around $50K-$100K annual premium spend.

Related work

For the broader contract-extraction pattern this builds on, see Contract review and clause extraction. For tracking renewal dates across the portfolio, see Lease and vendor renewal tracking. For the document-extraction pattern that powers the policy text extraction, see Extract structured data from PDFs. For the broader risk-and-compliance lens, see AI risk assessment for legal and compliance teams.

FAQ

Should we trust AI extraction for something as legally consequential as insurance coverage?

The AI handles extraction, not legal interpretation. The structured data (limits, dates, named insureds, deductibles) extracts reliably; the legal meaning of specific exclusion language is something to validate with a human reviewer (broker, lawyer, fractional risk manager). The pipeline produces a structured starting point; it doesn't replace human review on material policies. Treat the output as a draft analysis, not a final opinion.

What if our policies have endorsements and riders that change coverage substantially?

Extract endorsements alongside the base policy. The schema should explicitly include an "endorsements" array per policy, each with its own extracted fields. Modifications to the base coverage live in endorsements; missing them produces inaccurate analysis. The extraction prompt should be tuned to recognise the endorsement-vs-base-policy structure most insurance documents use.

How is this different from what a good broker should already be doing?

Functionally overlapping. A good broker proactively analyses your coverage and surfaces gaps. The reality is that broker quality varies; many brokers do good initial-placement work and less rigorous renewal-cycle analysis. The AI pipeline doesn't replace a good broker; it provides independent verification and the buyer-side analysis that informs the broker conversation. Teams with great brokers find the pipeline confirms what the broker already said; teams with mediocre brokers find the pipeline surfaces things the broker missed.

Can we use this for personal insurance — auto, home, umbrella?

Yes, the same pattern works. Personal insurance is usually simpler and less consequential than commercial, so the leverage is lower. For high-net-worth individuals with complex coverage (multiple properties, excess liability, art, watercraft), the analysis pays off. For typical personal portfolios, an annual review by your agent is usually sufficient.

What about international operations and multi-country policies?

Country-specific complexity is real. The extraction handles the document content fine; the analysis requires understanding which jurisdictions the policies actually cover, regulatory differences (e.g., cyber-disclosure requirements vary by country), and currency / limit-equivalence. For multi-country operations, the pipeline produces the raw extraction; the gap-analysis benefits from a risk adviser familiar with the relevant jurisdictions.